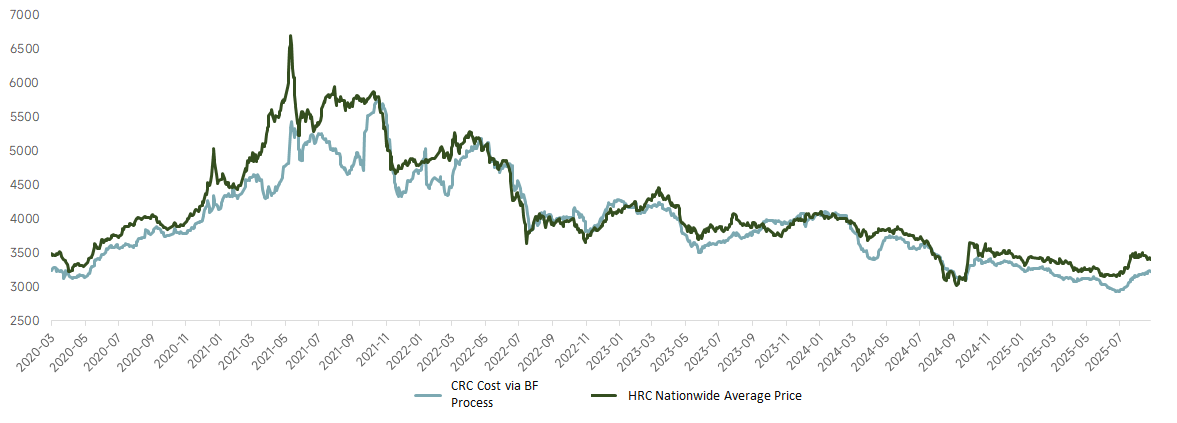

Part I: HRC Market Review in 2025

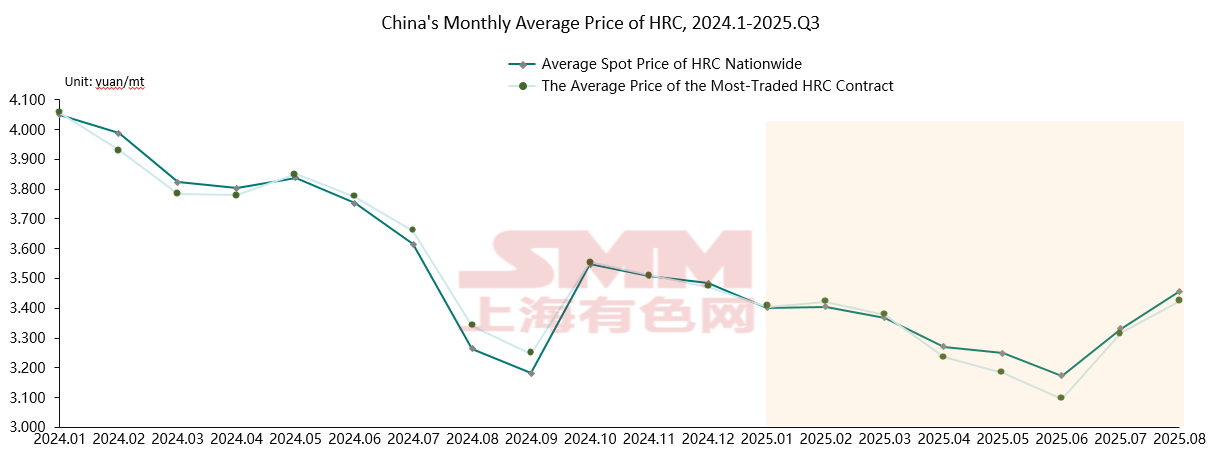

As of August 28, 2025, the national average spot price of HRC stood at 3,329.55 yuan/mt, while the average price of the most-traded HRC futures contract was 3,304.16 yuan/mt. From January to August 2025, HRC prices exhibited a "V"-shaped trend, with the year's low point occurring in June.

Compared to 2024, China's average spot HRC price declined by approximately 9%, while the average price of the most-traded futures contract fell by around 10%.

Supply side, HRC capacity additions from January to August 2025 fell short of expectations, with only three new HRC production lines commissioned (involving 10.58 million mt of capacity).

Production-wise, output during the January-August period was slightly lower than 2024 levels. This was partly due to higher impact from maintenance on HRC production in Q2, and partly because steel mill profits improved significantly this year, enabling more flexible production adjustments and resulting in lower-than-expected HRC output.

Demand side, from a micro perspective, as of the beginning of this week, the weekly average processing volume of HRC in mainstream warehouses in east and south China increased 11% YoY compared with the same period in 2024.

HRC apparent demand, as of last weekend, averaged 3.3362 million mt in China, versus 3.3416 million mt in the same period of 2024, down 0.2% YoY, indicating HRC demand remained in the doldrums compared with 2024.

In July 2025, China's indirect steel exports totaled 12.5607 million mt, up 4% MoM. From January to July, the cumulative indirect steel exports reached 81.2907 million mt, up 19% YoY.

By sector, from January to July, the machinery industry's indirect exports totaled 34.2026 million mt (up 18% YoY), steel product exports stood at 23.9532 million mt (up 21% YoY), and exports of motorcycles, bicycles, and related products amounted to 4.7368 million mt (up 32% YoY).

In September,

The impact from maintenance on HRC production was temporarily at 400,000 mt, down 350,000 mt MoM from this month, with maintenance observed at steel mills in northeast, north, east, south, and central China.

Considering some maintenance impacts remain uncertain, HRC production may continue to fluctuate rangebound under mill maintenance in September, with limited room for growth, indicating a neutral-to-slightly-bullish supply outlook.

In August, most industries entered the off-season, with construction and production pace slowing further due to weather impacts, and some manufacturers implementing high-temperature holidays.

Looking ahead, August remained affected by off-season factors, with overall operating rates weakening further. However, September marks the beginning of the September-October peak season, and as weather-related disruptions ease, enterprise operations are expected to gradually normalize, with downstream operating rates likely to increase slightly.

**Iron ore**: In early September, after the production restrictions for the military parade ended, hot metal output is expected to rebound rapidly, supporting iron ore prices. In mid-to-late September, pre-holiday restocking demand may drive ore prices slightly higher. Overall, iron ore prices are expected to hold up well in September.

**Coking coal and coke**: The earlier impacts of "anti-rat race" competition and safety inspections have gradually weakened. Recently, online auctions showed mixed performance, with some coal varieties failing to sell. However, frequent mine accidents recently, coupled with slow production resumptions at previously idled mines, have limited significant supply growth for coking coal. Mines remain reluctant to budge on prices, leading to passive rangebound fluctuations in the short term. In September, policy changes and hot metal trends warrant attention.

HRC prices have upside potential in September, with the most-traded contract expected to range between 3,330-3,580.

![[SMM Steel] SMS Group wins SAIL Durgapur billet caster modernization project](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)

![[SMM Steel] US drawn wire exports rise 12.5% MoM in January 2026](https://imgqn.smm.cn/usercenter/VgxkU20251217171719.jpg)

![[SMM Steel] Eurofer urges EU to act fast as global steel overcapacity hits record 2.4 billion mt](https://imgqn.smm.cn/usercenter/exdqc20251217171717.jpg)